2020 Quarter 3 Commentary

Quarterly CommentaryThe May Barnhard Investments team offers quarterly market commentary as a complimentary service. To learn more about our financial planning and investment services, contact us via the form below.

"The stock market is the story of cycles and of the human behavior that is responsible for overreaction in both directions.” - Seth Klarman

We hope all is well with you and your family and that you are staying safe and healthy. The markets around the world have continued to recover in the 3rd quarter of the year. All three major indices, the Dow, S&P 500 and Nasdaq, were in the positive territory for the quarter. The high-flying technology-oriented Nasdaq index experienced a correction (i.e. decline of more than 10%) in September, but half of the losses were regained by the end of the quarter. As we reported in our 2020 Q1 and Q2 commentary, “growth” oriented stocks have continued to outperform their “value” counterparts. We expect this trend to continue in the near future.

The table below summarizes the performance of various domestic equity categories over the past 3-month, 12-month and 3-year periods.

The U.S. equity markets continued to outperform most of the major developed economies in the 3rd quarter of this year. Developed markets, as measured by the MSCI EAFE Index, were up +4.27% for the quarter (-7.18% year-to-date). Emerging markets as a group increased by +9.05% for the same time period (-1.35% year-to-date) as reported by the FTSE Emerging Markets (EM) Index. Chinese companies represent more than 45% of the FTSE EM Index which is one of the main reasons for relative outperformance when compared to developed non-U.S. markets. Chinese stocks, as a group, were up +15.80% for the year as measured by the MSCI China Index.

We remain quite pleased by the market performance over the past six to seven months of the year. As a reminder, the major domestic stock indices were down as much as -36% by the middle of March. There were very few people who predicted or even suggested that such a recovery would be possible given the unprecedented and historic market volatility due to the coronavirus pandemic. This serves as a great reminder of how quickly and rapidly the public can change its “collective mind” and move in the opposite direction. We remain committed to our long-term investment strategy that is based on a thorough understanding of our clients’ financial goals and cash needs. We believe this approach is best suited for today’s markets.

One of the more notable announcements in the 3rd quarter related to the change in how the Federal Reserve Bank (the Fed) would evaluate when to raise short-term interest rates. In short, it will be looking for three conditions to consider a rate hike: significant improvements in the unemployment rate, inflation on track to the 2% target and enough evidence that it would stay above the target for a reasonable duration. It will likely take some time to see the actual impacts of this change. It would be fair to assume that our current historically low interest rates will remain in place at least until 2023. This is important for those of our clients who require or prefer to maintain a significant percentage of their portfolio in fixed income investments such as bonds, money market funds or certificates of deposit (CDs).

The chart below summarizes the Fed rates from 1970 to 2020.

To potentially reduce the negative effects of the ultra-low interest rates on those who need income from their portfolios, we suggested three potential options that include preferred stock, total return and multi-sector bond funds and dividend-paying stocks that have a history of increasing their dividends. These options have been discussed in detail in our investment webinars. Depending on your specific risk tolerance and time horizon, all or none of these strategies may be appropriate for you. One of our immediate objectives is to be proactive and make our clients aware of other options that may be more advantageous in today’s markets.

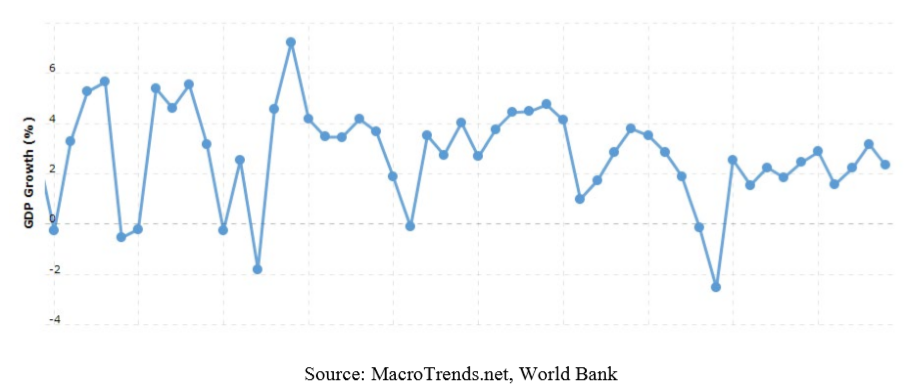

As some of you may recall from our previous market commentaries and webinars, we developed a framework of three core scenarios that we considered as an outcome of the coronavirus pandemic. One of the scenarios in this framework, the “bear” case, called for a double-digit decline in the U.S. GDP. This case was based on prolonged nationwide shutdowns that would last for several months or even longer. Based on what we learned about the virus, it is unlikely that such a scenario will come to fruition. The Fed estimates the U.S. GDP to decline by -3.7% in 2020 and increase by +5.0% in 2021. The range reported by other major financial institutions is between -3.8% and -5.5% for 2020 and between +2.9% and +6.1% for 2021. These estimates are consistent with our “base” case scenario which we currently apply to our investment decisions. Feel free to reach out to us if you are interested in discussing these scenarios in more detail.

The chart below summarized the U.S. GDP growth from 1970 to 2020.

The overall unemployment rate, and more importantly the projected and actual changes in the number of unemployed people, has been one of the main discussion points of many economists and financial professionals. The official unemployment rate is down from 14.7% in April to 7.9% in September of this year. Given the anticipated structural changes in our economy, it is unlikely that we will see this rate approach the February percentage of 3.5% any time soon. We believe this metric is important for the purposes of evaluating the direction of our economy and certainly has some impact on the direction of the equity markets. However, other factors such as interest rates may have significantly more impact on the stock markets. As a result, we suggest that our clients refrain from making any significant portfolio allocation decision based solely on their perceptions of the economic recovery and unemployment rates.

As many of you know, markets are always “forward looking” and quickly adjust for most anticipated changes in the GDP growth, unemployment rates, corporate earnings etc. These adjustments are not always precise in the short-term and the actual effects are mostly seen after a few or even several years. As Benjamin Graham famously said that “in the short run, the market is a voting machine but in the long-term, it is a weighting machine”. There will always be market shocks and we need to be prepared to take advantage of such opportunities. Again, this is one of the reasons why we strongly recommend that our clients have a financial plan and focus on their long-term financial goals.

Our market commentary would not be complete without at least some of our thoughts on the upcoming Presidential election. We fully recognize that equity markets tend to be more volatile in election years. What is different in this election cycle is that many investors anticipate most of the volatility to happen after November 3rd. Depending on the preliminary results and the spread between the candidates, one of the parties may ask for the ballot recount or even contest the entire outcome. The markets are not likely to react positively to such events.

The effects of the election on the markets have been discussed and thoroughly researched by many in the financial industry. In fact, we have been spending considerable time to review the most recent polls and better familiarize ourselves with the agenda of each candidate. Our conclusion is relatively simple. In the past, the President’s political party itself had limited impact on the market performance results. The chart below summarizes the performance of the S&P 500 Index based on the President’s political party.

We note that “event driven” investing has not been a reliable way of managing money, especially when people make such decisions based on their emotional and/or political views. We are not implying that you should do nothing. In fact, we have been diligently adjusting the allocations in our managed portfolio to better position them for more market volatility later this year, regardless of the reason for such turbulence. In our experience, gradual adjustments are usually more beneficial to the health of your portfolio than any drastic changes that are based on subjective opinions of what may happen in the future.

As we are reaching the end of this difficult and historic year, we will be focusing more on financial planning ideas that affect your portfolio and overall financial plan.

Thank you and stay safe and healthy!

Questions about this post? Please complete the form below.