2022 Quarter 3 Commentary

Quarterly CommentaryThe May Barnhard Investments team offers quarterly market commentary as a complimentary service. To learn more about our financial planning and investment services, contact us via the form below.

“I remember the $0.05 hamburger and a $0.40-per-hour minimum wage, so I’ve seen a tremendous amount of inflation in my lifetime. Did it ruin the investment climate? I think not.” - Charlie Munger

Our third quarter market update may sound familiar to our readers that have been following the Quarterly Commentary over the past few updates, because many of the same macroeconomic trends have continued to persist since our previous update. The Eastern European conflict continues to escalate and may intensify given Russia’s cut off of critical gas infrastructure to Europe and annexation by referendum of certain occupied territories of Ukraine by Russia. Inflation continued to inch higher despite continued efforts from the Federal Reserve to increase interest rates and decrease the balance sheet in a process called quantitative tightening. Central banks around the world have followed suit, also implementing tighter monetary policy for their respective currencies. In a potential show of global weakness, the dollar strengthened against foreign currencies and global supply chain issues have continued to persist. Themes of protectionism have also manifested in protectionary and anti-immigration policies that may exacerbate some of the global supply chain issues.

In this quarter’s update, we explore how these trends are affecting equity and fixed income markets. We also delve into how individual investors can avoid bear market pitfalls with tried-and-true investor strategies. Finally, we take a look into MBI’s own strategies for navigating the investing waters during these perilous times. We believe that despite these circumstances, the patient, prolonged investor can find great value and protect their assets for the long run.

Equity

Recent continuation of previously mentioned macroeconomic trends and events (global inflation, tight monetary policies by central banks, etc.) have meant the equity markets’ soft start to the year continued throughout Q3. July seemed promising when the S&P rebounded to return +9.2% in the month; however, the Cboe Volatility Index (VIX), which measures market volatility, has been trending higher since mid-August. Market ripples from the Fed rate hikes, inflation uncertainty and policy response mean investors saw a reversal in these gains and may have to brace for continued market volatility throughout year end.

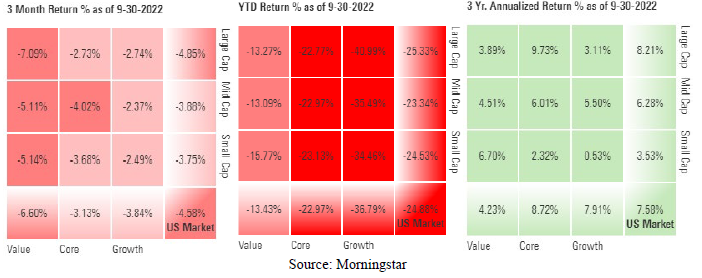

Below, you’ll find the performance of various domestic equity categories over the past 3-month, 9 month and 3-year periods.

As indicated in the charts, over the past year we’ve seen more volatility in growth funds specifically compared to the value category. While this has not changed in the recent quarter, Q3 slightly bucked this trend. Year-to-date, growth funds have significantly underperformed value equities.

Sector-wide, the only gains have been seen are in the consumer discretionary and utilities sectors over the past quarter. Overall, energy is the only sector posting sizable gains year-to-date. The biggest drops over the past three months have been materials and communication services. As a whole, most sectors are down year-to-date, and we continue to advise portfolio strategic adjustments to take advantage of the market volatility based on your circumstances.

Good news for investors is that despite the previously mentioned continued volatility, the most recent quarter remains relatively less precarious than its Q1 and Q2 counterparts. As seen in the following graph, Q3 has seen more abundant neutral and positive closing days, as well as less frequent negative days. These numbers still pale in comparison to the median 2019 – 2021 returns but remain a step in the right direction of dampening the current year’s market volatility.

Fund managers, individual investors, and other market participants are looking for yields in equity in non-traditional areas. International equities have underperformed domestic year-to-date, and many fund managers predict continued underperformance given questions about the strength of the dollar and economic uncertainty. Some investors are considering Real Estate Investment  Trusts, otherwise known as REITs, to receive relatively predictable above-average income. Others are looking to preferred stocks, which, although equity-like, typically have more characteristics in common with their fixed income counterparts.

Trusts, otherwise known as REITs, to receive relatively predictable above-average income. Others are looking to preferred stocks, which, although equity-like, typically have more characteristics in common with their fixed income counterparts.

One type of equity that has performed relatively well over the past year compared to peers, have been dividend stocks and dividend growth stocks. Investors may receive compensation for holding equity securities in the form of either capital gains, or an increase in stock price, or through dividends. This type of equity promises less volatility, while still delivering much sought-after yield.

Dividend appreciating stocks and stock funds have become increasingly popular over the past year. The S&P 500 index pays out 2.2% in dividends. Dividend appreciation stocks focus on companies with solid growth fundamentals, that not only pay out dividends, but are positioned to continuously increase these payments over future years. Depending on your specific situation and preferences, the equity portion of your portfolio can be adjusted to yield anywhere between 3% to 5% by focusing on companies that pay dividends.

Fixed Income

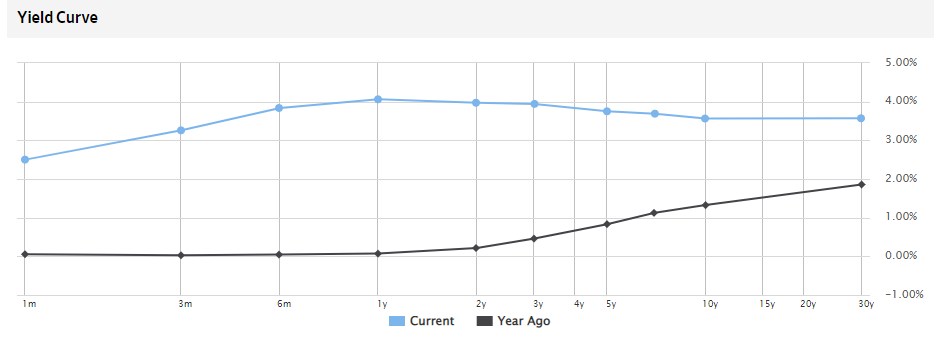

Over the past year, yields on Treasury bonds have increased significantly. In particular, short-term yields have increased to over 4%, levels not seen previously since 2007. Federal Reserve actions have also altered the shape of the yield curve as well, with short-term yields increasing more than their long-term counterparts. Conceptually speaking, the short end of the curve is influenced by the Federal Reserve actions. In contrast, the long end of the curve is impacted by economic outlooks from market participants. Given this, it’s not surprising that recent Federal Reserve actions have resulted in the shape of the curve we see today. Should the Federal Reserve reverse its trend and lower interest rates, we may see short-term rates lower below long-term rates again.

Below, we’ve included the yield curve comparison from the previous year to the current year. As mentioned, note how short-term rates have increased significantly more than long-term rates in the same time period.

One of the most frequent questions and important discussion points is on the relationship between inflation (CPI) and the Fed interest rate policy. Understanding there are many variables that impact this relationship, we would like to point that historically the Fed Funds rate peaked at the end of the inflationary cycle. With inflation at 8.3% and the Fed rate at 3.25%, there is still some room for the two metrics to converge. As a result, we expect more volatility until this happens. See below for details.

Depending on how inflation reacts to the current hikes, the Federal Reserve could continue to hike rate for the foreseeable future, or reverse course due to market reaction to the rate hikes. Their course of action remains to be seen.

Housing

As interest rates increase, so do mortgage rates, historically resulting in lower sales and potentially lower prices. Consumers are already noticing decreases in the sales prices. U.S. existing home sales have decreased significantly since pandemic-related high.

As a result, rents have soared in recent months. Instead of dropping prices for their homes, sellers are more often than not opting to rent out their property to others until they are ready to sell. This further decreases the number of homes being sold in the current market.

In terms of the broader economy, increased mortgage rates and decreased prices could contribute to deflationary pressure, given that housing contributes to inflation (CPI). The Fed Chairman, Jerome Powell, has specifically spoken about cooling off the housing market during his public appearances, noting that a correction in the housing market would make home ownership more affordable for many. Additionally, a decrease in home sales and turnover may affect other real-estate related industries, such as home building, furniture, home improvement retailers, etc. that tend to see increased sales during times of housing booms.

Investing Strategies

Despite the relatively volatile market performance over the past quarter, we would like to remind you that investors’ long-term performance is largely driven by individualized actions in bear markets. Investors that excessively trade during times of bear markets tend to underperform when compared to their more “passive” counterparts.

Bear markets can certainly be intimidating for investors; however, many also tend to overestimate the length of time that such markets occur and underestimate how rapidly the recoveries happen. On average, bear markets have lasted eleven (11) months – less than a year. Additionally, on average, the length of time it took for stocks to recover to their previous highs was nineteen (19) months. See charts below for additional details.

Markets also tend to turn around faster than investors realize. Historically, the average return is actually 14.8% the year after the S&P enters a bear market territory.

Investors have tools at their disposal to take advantage of these market fluctuations, rather than run from them. Dollar cost-averaging (DCA) is perhaps the most important tool. Any purchases that you make while the markets are down, potentially make it more advantageous for the long-term focused investor to enter the market at a more attractive point (i.e., buy low). Furthermore, the greater the volatility, the greater the potential gain for those with above average risk tolerance. In fact, as you can see on the chart below, bear markets historically have been a great entry point for investors, per the S&P 500 index returns.

Portfolio Strategy

As part of our quarterly procedures, we plan to adjust some of our managed accounts in accordance with each clients’ individual investment policy. There are some strategies that we plan to implement across all client portfolios, including a continuation of tax loss harvesting strategies whenever possible. As previously mentioned, this approach allows investors to offset their capital gains, if any, or carry forward unused losses to future years while staying invested with their overall asset allocation.

In our previous commentary, we mentioned that in some portfolios, specifically those with above average risk tolerance as well as longer time horizons, we increased the allocation to domestic large cap growth equities. Results have been generally positive relative to other asset classes. We will continue to monitor this strategy into the future but believe that the long-term outlook of large-cap domestic equities remain attractive. Based on current market and economic conditions, we remain neutral on mid-cap and small-cap domestic equities.

We will continue to underweight our international allocations in most of our managed portfolios. Global macroeconomic trends do not currently present a bullish case for international stocks, in particular due to currency fluctuations and energy related issues. One of the considerations is the fact that many domestic multi-national companies provide exposure to international markets and, as a result, inherent portfolio diversification. We also believe that the continued strength of the dollar adds increased foreign exchange risks to these securities in the near term.

We are closely monitoring our fixed income allocation for changes to our overall recommendations on: 1) duration: and 2) credit quality. Currently, we maintain a mix of different fixed income types, including Treasury, corporate, securitized, and high yield bonds, depending on the investment policy of each client. We continue to mostly focus on shorter duration bonds with higher quality. The Fed’s decisions will likely impact the opportunity for a pivot to longer term fixed income options, whereas the overall economic profile will influence the credit quality in our portfolios.

Thank you and stay safe and healthy!

Questions about this post? Please complete the form below.