Charitable Donations: Smart Strategies for Giving

Investment Insightsby Jenny (Zhen) Wang, CFP® , CFA® and Senior Financial Analyst Yunen Ding*

*Jenny and Yunen were respectively a portfolio manager and senior financial analyst at MBI.

Since there are various ways of encouraging you (well-wishers or donors) to channel resources toward charitable organizations, here we will cover three strategies that help you save taxes while utilizing your money for good.

Donating Appreciated Securities to a Charity

If you have securities with large amounts of unrealized capital gains in your taxable accounts, you may consider donating them directly to charity, instead of selling them and donating the cash proceeds. This will allow you to bypass capital gains tax and deduct more charitable contributions. The chart below can serve as a good example to illustrate the tax benefits. Assume you would like to donate $100,000 worth of securities with a $50,000 cost basis to your favorite charity and your effective income tax rate is 28% and capital gains tax rate is 15%. You will receive extra $9,600 ($28,000 - $18,400) of net tax savings. You will end up donating the full $100,000 amount instead of $92,500 ($100,000 - $7,500 of capital gain tax) to the charity.

Donor-Advised Fund

Donor-advised funds (DAFs) have become a popular donation option in recent years because of their relatively low costs and ease of use. DAFs are a tax-advantaged investment account offered by many financial institutions like Schwab and Vanguard, where you can contribute appreciated investments so that you do not need to face the tax consequences of selling them. The beauty of DAFs stems from that you obtain immediate tax deduction for the year you make the contribution, and your contributions continue to grow tax-free in the account. You will still have some levels of control over the investment activities in the account and you get to choose the donation amount and pick any IRS-approved charity of your choice in any following year. Since the funds stay invested until you make a grant, you may have even more to donate than when you funded the account.

Charitable Remainder Trust

In December 2019, Congress passed the SECURE Act which includes many reforms that make savings for retirement more accessible. However, there is one potential downside, that it eliminates the “Stretch IRA” strategy which allows non-spouse IRA beneficiaries to stretch the required minimum distribution (RMD) over their lifetimes. Effective January 1, 2020, for IRAs inherited from original owners who passed away after December 31, 2019, the new rule requires beneficiaries to withdraw the proceeds within a window of 10-years. This new rule does not apply to the following groups:

- Spouse or minor children (until they hit age of majority)

- Disabled beneficiaries

- Chronically ill beneficiaries

- Someone <10 years younger than deceased

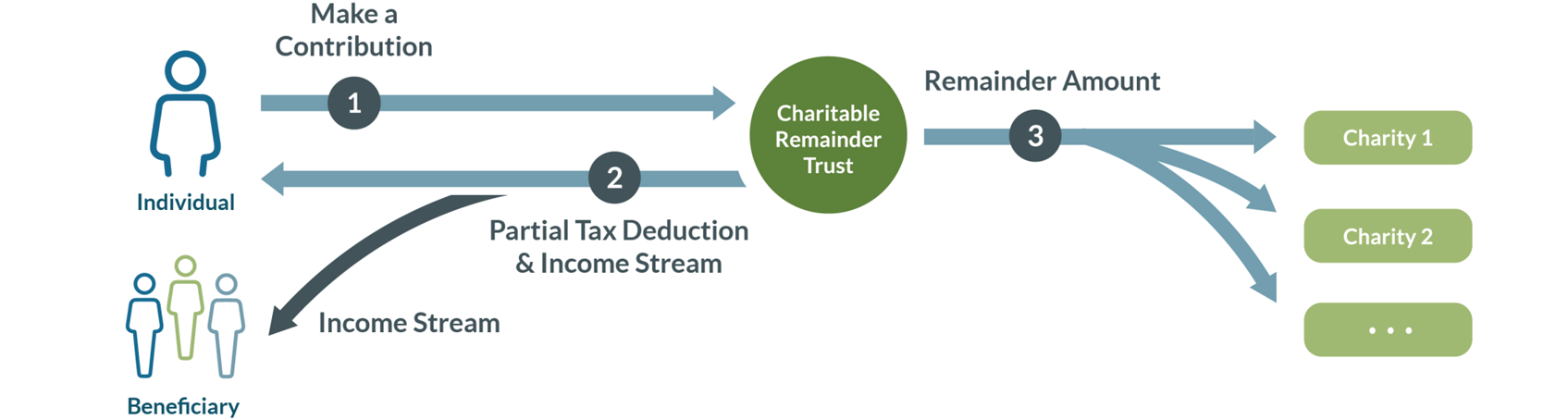

As an alternative, a Charitable Remainder Trust (CRT) is an irrevocable trust that distributes an annual income to donor and/or beneficiary(ies), either for life or for a term of not more than 20 years. At the end of the life (or term), the remaining trust assets are paid to charity(ies).

Source: Fidelitycharitable.org

There are two types of CRTs, Charitable Remainder Annuity Trust (CRAT) and Charitable Remainder Unitrust (CRUT). CRAT distributes a fixed annuity amount each year. The annuity amount will be a fixed percentage (at least 5% but no more than 50%) of the initial value of the property transferred to the CRAT. In contrast, CRUT pays out a fixed percentage of the trust value each year. For either type, the assets will only be taxed when they leave the trust and the donor will receive an immediate income tax charitable deduction when the CRT is funded based on the present value of the projected remainder interest that passes to the charity. See below for some key benefits of CRTs:

- Converts appreciated assets into lifetime income for donors or beneficiaries

- Preserves the value of the assets and no capital gains tax generated from the sale of assets

- Reduces donor’s current income taxes with chartable income tax deduction

- Reduces or eliminates donor’s estate taxes

- Helps with one or more charities

If you have a passion for charitable donations and would like to learn more about smart donation strategies, we will be happy to offer our expertise to help you to achieve your goal. Reach out to our professionals via our contact form.

Questions about this post? Please complete the form below.